Former DTC Chairman and CEO William F. Jaenike writes about…

The Big Shifts In Share Ownership that Created a “Paperwork Blizzard” in the late 1960’s… Early Efforts to Deal With The Crisis…

The Formation of BASIC, the Banking and Securities Industry Committee…

The Formation of the Depository Trust Company…

Other Important Developments, such as CUSIP, “Machine Readable Stock Certificates”, Uniform Forms, Automated Transfer Instructions, the Direct Mail Program, Omnibus Proxies, FINS and the Rise and Fall of Regional Depositories

Big Shifts In Share Ownership Create A “Paperwork Blizzard” That Buries the Securities Industry in the late 1960s

During the 1960s the American capital markets began to move, rather rapidly, from being largely retail-investor-oriented to being increasingly dominated by large financial intermediaries and institutional investors – pension funds, mutual funds, insurance companies and bank trust departments.

Post-trade processing changed radically as a result: Brokers had to deliver rapidly increasing numbers of physical stock certificates to the institutions’ custodian banks, versus payment, instead of simply holding the certificates in the brokers’ own “street name” in their own vaults, or mailing them out, typically at their leisure, to individual stockholders who wanted to have them. [In those days, it is important to note, most banks, and virtually every insurance company and mutual fund in America was prohibited – in some cases by their own sense of their fiduciary duty, in some cases by customer requirements and in many cases by law – from paying out money to “settle” a securities transaction until the security itself was ‘in hand’, and in ‘good form’].

Concurrently, trading volume soared to a then-staggering 20 million shares a day. (That was a mere 1% of today’s volumes - on just a so-so day for stock markets of the 21st century!)

Brokers’ “back-offices” – often disparagingly but aptly called “the cages”, since they and their workers were indeed behind bars - could not keep up with the resulting paper deluge. Hundreds of thousands of transactions remained unsettled every day due to “fails to deliver”. And these “fails”, as they were called, caused many millions of dollars in dividends to be issued and sent to the wrong parties each quarter, because the ownership could not be transferred, and registered “on the corporate books” in time to make the “record date”. The backlogs, delays, clerical errors, rejections and the re-processing steps that arose also led to hundreds of mil- lions worth of physical certificates being lost or stolen as they batted back and forth among the overworked and totally overburdened participants. And, as the BASIC researchers later discovered, the same items were being handled over and over again before final- ly being delivered correctly, and “in good order”, which contributed even more volumes to overburdened systems - and further over- burdened them with uncountable layers of added costs.

The NYSE and other stock markets had to close on Wednesdays, and other days saw shortened trading hours in order to lighten the work load on the back-offices and give them a chance, in theory at least, to “catch up” with the backlogs. These Draconian measures were not enough to prevent the demise of some prominent firms – most notably Goodbody and F.I. DuPont – not to mention many other smaller firms that closed or that were merged out of business.

In short, by 1968 the nation’s capital markets were being brought to their knees. The media had a field day reporting on the impend- ing catastrophe that was set to befall the Wall Street Titans, with little or no coverage, by the way, of the potential impact on aver- age American investors.

During the run-up to this crisis period, several industry committees were formed to deal with the impending chaos that virtually everyone in the business knew was coming:

In 1964, the American Bankers Association (ABA) formed the Committee on Uniform Security Identification Procedures (CUSIP) to develop a standard code for identifying security issues, of which there were a million or so, most of them municipal bonds.

In 1966, the Security Imprinting and Processing Task Force (SIP) was formed, to develop more uniform, and ideally, machine-readable securities certificates.

In 1968, a Joint Industry Control Group had co-chairmen (they were only men in those days) from both the banking and securities industries in New York, with subcommittees covering Delivery Problems, Transfer Problems and Dividend Problems, among others.

In 1969 and 1970 many consultants were hired by various industry organizations to study solutions to the crisis, including such then- big names as Arthur D. Little; North American Rockwell; Lybrand, Ross Bros. and Montgomery; and the Rand Corporation. Various recommendations came out of these studies including the idea of a Transfer Agent Depository (TAD) which proposed that brokers deal directly with transfer agents and where “bookkeeping positions” would serve to replace physical certificates. While conceptually interesting, and theoretically a cure for the paperwork crunch, the TAD approach never gained much traction. There were (and are still) many hundreds of transfer agents and the vast majority were not technologically or procedurally up to the task, or - far more importantly - willing and able to invest the needed money to get there. Nor were the brokers for that matter.

One of the most influential events, in terms of giving the crisis the high level of attention that was urgently needed, was a September 1969 speech by Ralph S. Saul, President of the American Stock Exchange and a former Director of the SEC, to the Securities Industry Operations Conference in which he called for a high level inter-industry committee to deal with the morass of proposals which had generated so much interest but so little action.

Thus, the seed was planted for the formation of BASIC, the Banking and Securities Industry Committee, comprised of CEOs from both industries.

Walter B. Wriston, Chairman and CEO of then First National City Bank, and another founding member of BASIC, wryly related a call he got from Saul, pointing out that much of the crisis was due to two-week backlogs of un-transferred certificates at transfer agents, including Wriston’s own. (Transfers were supposed to be completed in two business days, according to NYSE listing regulations.) Wriston said that Saul was certainly mistaken and invited him over for a tour of his transfer operation at 111 Wall St. They scanned the backs of certificates and Wriston found that Saul was indeed wrong – transfers weren’t taking 2 weeks. They were taking 3 weeks!

The Formation of BASIC – The Banking and Securities Industry Committee:

At the beginning of 1970, with Congress breathing down their necks and threatening to federalize post-trade operations, prominent Wall Street CEOs agreed on forming a Banking and Securities Industry Committee, very aptly known, in view of its agreed-upon approach, as BASIC. This was no small matter at a time when the then sacrosanct Glass-Steagal Act required a strict separation of Banking and Securities Industry activities - and when major banks and brokers basically distrusted and disliked one another - and where they were more engaged in pointing fingers and blaming the other side for the problems that were causing the “paperwork crisis” than in seeking solutions.

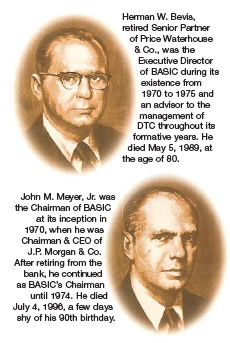

The BASIC Committee consisted of the Presidents/CEOs of the NYSE, AMEX and the NASD, and three Chairmen and CEOs representing the “New York Clearing House Banks”, where there were 11 member banks back then. In February, John M. Meyer, Jr., Chairman and CEO of Morgan Guaranty Trust Company, who had been elected as BASIC’s Chairman, induced his good and trusted friend, Herman W. Bevis, the recently retired senior partner of Price Waterhouse & Co., to serve as the Executive Director of BASIC.

Herman, as he was known to me and the rest of his staff, insisted on serving pro bono – in part to drive home his independence and objectivity, in part because his partnership agreement required him to forego post-retirement “employment” - and in the largest part because Herman was a genuinely “good citizen”, and a tireless worker, who was truly attracted by the enormous challenge. (A ‘well-earned’ donation to a charity of his choosing – Greenwich Hospital - was made after the Committee was officially dissolved).

Herman, as he was known to me and the rest of his staff, insisted on serving pro bono – in part to drive home his independence and objectivity, in part because his partnership agreement required him to forego post-retirement “employment” - and in the largest part because Herman was a genuinely “good citizen”, and a tireless worker, who was truly attracted by the enormous challenge. (A ‘well-earned’ donation to a charity of his choosing – Greenwich Hospital - was made after the Committee was officially dissolved).

He soon chose a BASIC “Task Force” – the staff – consisting of six promising young executives from BASIC’s sponsoring firms to do his fact gathering and to help analyze the feasibility of the various proposed solutions to the paperwork crisis that were being advanced - along with the numerous reports from prominent consulting firms that were circulating around the industry, as mentioned above.

BASIC’s organizing meeting was held on March 11, 1970. Its members were:

John M. Meyer, Jr., Chairman

Herman W. Bevis, Executive Director

Robert W. Haack

William H. Moore

Ralph S. Saul

Richard B. Walbert

Walter B. Wriston

Affiliation

Chairman, Morgan Guaranty Trust Company

Retired Senior Partner, Price Waterhouse & Co.

President, New York Stock Exchange

Chairman, Bankers Trust Company

President, American Stock Exchange

President, NASD (Walbert soon retired and was replaced by Gordon S. Macklin)

Chairman, First National City Bank

By June 1st, the BASIC Task Force had been recruited as follows:

Peter C. Campbell Arnold Fleisig

David Fuchs

Carl T. Hagberg

William F. Jaenike

Milan S. (Steve) Soltis

Affiliation

Price Waterhouse & Co.

NYSE (formerly of Bache & Co.)

NYSE

Manufacturers Hanover Trust Company

AMEX

Chase Manhattan Bank

Concurrently, both Houses of Congress, in consultation with the SEC, drafted legislation to deal with the paperwork crisis. Sen. William V Roth (R) of Delaware considered a Federal corporation to replace the various clearing corporations and depositories serving the stock exchanges in New York and other market centers. Along with the Senate subcommittee, a House subcommittee under Chairman John Moss (D) of Sacramento, held hearings on the matter. BASIC played a major role, testifying at those hearings and assuring Congress that the crisis could and would be solved in the private sector, given some time. BASIC’s main proposal was a national system of linked depositories with open access for all financial institutions but especially banks and brokers.

To drive home its openness to other regions of the country and to show that BASIC was not proposing a New York-based monopoly, designed to drive regional banks and brokers out of business, BASIC collaborated with the exchanges and bankers in Chicago and San Francisco to form a sort of national version of BASIC that came to be called by the big mouthful, “National Coordinating Group for Comprehensive Securities Depository Systems” (NCG for CSDSs…or, as the BASIC task force irreverently called it, mainly for want of anything better to call it for short, “Nickachizdizz”). Persuaded by BASIC’s commitment, its openness to regional access and the considerable “heft” of its high-ranking membership, Congress postponed further intervention to give BASIC time it needed. Congress eventually dropped the idea of intervening.

BASIC’s efforts were helped by the success of the Federal Reserve Bank of NY’s book-entry system for U.S Treasuries, introduced in the late 60s and early 70s. That success convinced the Fed’s bank members, and the brokers who had access to the system through member banks, that BASIC’s proposal was on the right track. (An interesting historical sidelight; the birth of the Fed’s system had been hastened dramatically by a series of shocking incidents, where kids in sneakers were mugging Wall Street’s famously old and rickety “runners” as they carried millions worth of Treasury bearer certificates through the canyons of lower Manhattan for delivery to banks and brokers…and literally running off with the loot themselves).

By early 1971, the BASIC Task Force had analyzed many thousands of stock deliveries and concluded that almost all of them could be replaced by a depository’s book-entry system. The immediately obvious choice for the system was the nascent Central Certificate Service (CCS) of the NYSE. CCS had a number of false starts in the late 60s, but by the early 70s it was used by many brokers as their “vault” - and by several New York banks as a place to hold the collateral behind brokers’ collateral loans, that could be made by “book- entry pledges” to the banks at their CCS accounts, instead of having to move physical stock certificates to physically “post” such collateral. The real key to the success of CCS, however, would be the banks’ willingness to accept book-entry deliveries vs. payment from brokers to settle securities trades, thus eliminating the brokers’ daily need to withdraw ten of thousands of physical certificates from CCS’s strained certificate inventory each day in order to make DVPs.

Under strong encouragement from BASIC, the New York banks, joined by a few large banks outside New York, came up with a stop- gap procedure by which they would accept CCS book-entry deliveries from brokers and immediately instruct CCS to put the stock into transfer and deliver the new bank-nominee-name certificates to the banks for entry into their vaults – essentially a replica of their regular way of doing business, but where CCS could take over the custody, inventory-assembly, transfer-prepping and transfer-monitor- ing and delivery processes . This breakthrough solved the immensely difficult and costly need for urgent (same day) withdrawals from CCS by brokers.

The Formation of the Depository Trust Company:

With credibility now having been gained in both New York and Washington, DC, BASIC pressed on with its plan to “spin-off” CCS from the NYSE. As I look back, I continue to be amazed by the complexities of the numerous legal, regulatory and practical issues that had to be dealt with…and by the sheer brilliance, and unsurpassed political skills that Herman employed to move things along so quickly and so effectively.

Herman’s master-plan – and ultimately BASIC’s – was to convert CCS to a user-owned cooperative that was to become a New York State chartered “Limited Purpose Trust Company”. And also, thanks to cooperation from senior Federal Reserve System officials, it became a member of the Fed as well. These steps were designed to meet banks’ fiduciary needs for properly and legally “safekeeping” their customer securities - and so the Depository would be able to move very large sums of money, safely and quickly - and, of course, to provide a strong regulatory framework that would pass muster, and inspire confidence in all 50 states.

While this was happening, BASIC completed negotiations with the NYSE for the “spin-off” including a multi-million dollar payment to the Exchange for its prior investment in CCS. One of its most-senior executives was reluctant to give up control of what was fast becoming its crown jewel, but pressure from BASIC and from many other powerful people forced his hand. At the same time, many of the prospective owners from the banking side – who had an absolute horror of potential unionization - were fearful of joining a “union shop”, which DTC was, and still is. And, whether due to Herman - or due to an even bigger fear that the federal government would step in to regulate the system if they didn’t step up to the plate - these fears were largely put to rest.

On yet another front, the Uniform Commercial Code (UCC) of many states required a securities depository to be owned by a stock exchange. More important, however, the UCC of many states (which was a far cry from being “Uniform” in all states, as its name implied) - as well as Insurance Company and Mutual Fund Regulations in a great many states – required the actual, “physical delivery” of securities before any money could be paid-out in “settlement” of a securities transaction. Many states also required the “physical safekeeping” of securities owned by banks, Insurance Companies and Mutual Funds that were incorporated in their states – and typically required that the securities be held by regulated custodians, who had to keep the securities within the state. (The law in Wyoming specified that securities needed to be kept in-state and “in a strong iron box”) Thus, BASIC’s “spin-off” plan – in order to attract the needed “critical mass” of depositors - included a nationwide lobbying effort to legalize a “book entry depository and settlement system.” While this was proceeding, BASIC arranged for the formation of CCS, Inc. – on March 31, 1972 – to begin the separation from the Exchange.

On June 1, 1972, at BASIC’s recommendation, the NYSE hired William T. Dentzer, Jr. as the CCS, Inc. Chairman and CEO. Dentzer was leaving as Superintendent of the New York State Banking Department and was unusually qualified in a number of respects for the CEO position.

After a series of legal, regulatory and organizational steps, including the election of a predominantly user board of directors, CCS, Inc. was converted to The Depository Trust Company on May 11, 1973 and Bill Dentzer became DTC’s first Chairman.

Herman’s intellectual and political genius was also evidenced in the ownership and governance provisions that were put in place for DTC. As a non-profit organization, share ownership was intended primarily to provide voting rights, and thus, to let interested users directly influence the company’s control and direction. DTC’s capital stock was quickly taken up by the founding banks and by many of the bigger brokerage firms, so gradually, the NYSE became a minority owner. DTC’s users had the option to buy in - based on the number and value of shares on deposit, and on average transaction numbers, in order to balance the rights of big bank depositors, with lots of shares, against those of brokers – with fewer shares on deposit back then, but typically with many more transactions. Stock ownership also came with cumulative voting rights, so that no single stockholder could dominate the board of directors and so the smaller members could pool their votes to ensure their interests were represented at the table. As a not-for-profit corporation, no dividend was to be paid to stockholders, thus avoiding double taxation. But any surplus funds would result in refunds to members, with appropriately lowered fees in subsequent periods.

Now DTC’s growth took off, exponentially. It very quickly grew to include several thousand stock issues – albeit with total shares worth less than ten billion dollars (which in those days was a very big number) held for 12 New York banks, nine banks in other states and 244 brokers…with some 50,000 book-entry deliveries on a busy day.

BASIC’s Task Force work was completed by the end of 1972 and its members returned to their employers, who had loaned them out. BASIC itself continued to meet regularly to monitor and assist DTC’s progress and to ensure that Congress remained satisfied with the work still underway. In 1974, BASIC decided its mission was complete and DTC was well equipped to take over any future inter-industry collaboration on its own.

Other Solutions to the Paperwork Crisis Studied by BASIC:

CUSIP: BASIC’s first action was to encourage the imprinting of the CUSIP number, mentioned above, on stock certificates. Simply put, CUSIP was needed to uniquely identify securities that often had similar issuers’ names which, for years, generated huge numbers of erroneous deliveries and incorrect computer record-keeping entries.

On April 2, 1970, members of BASIC’s Task Force met at the American Banknote Company with representatives of that company, the American Society of Corporate Secretaries, the Stock Transfer Association and the Corporate Transfer Agents Association. After inspecting many varieties of certificates they concluded that the space in the “open throat” (the blank space, essentially in the center of the stock certificate, where the name, and often the address of the registered owner was imprinted) was the only space that could accommodate the CUSIP number in all cases. Days later the NYSE recommended imprinting the CUSIP number in this location to its listed companies. They stepped up to the plate and endorsed such use of CUSIP even though they would incur considerable costs to imprint CUSIP numbers on their then very large inventories of blank stock certificates.

Meanwhile, Standard & Poor’s (S&P), operating under a charter from the American Bankers Association, had made a huge investment over half a decade by creating and printing a mammoth annual directory of stock and bond issues (most of it for hundreds of thou- sands of municipal bonds) with a CUSIP number assigned to each. Unless S&P could see a way to recover its on-going investment through sales of the directory it could no longer continue to wait, and to suffer losses all the while - to learn whether CUSIP would fly. Thus it might have to cease its CUSIP directory and related efforts. A sort of chicken-or-egg situation had arisen: the CUSIP number was needed by the receiver of a transaction but unless the authorities mandated CUSIP’s use, the originator of the transaction had no incentive to include the number in their instructions. Thus, S&P’s CUSIP directory could not be sold in quantity. A “crisis meeting” among all concerned parties was held on December 14, 1970. It led to action.

With BASIC’s encouragement, all exchanges, the NASD, the bank clearing houses, the Municipal Finance Officers Association, the Corporate Secretaries Society and the Treasury Department adopted rules and requirements that certificates delivered by banknote companies had to have the CUSIP number printed on them by October 1, 1970.

In early January 1971, the BASIC Task Force proposed an April 1, 1972 deadline for mandatory use of CUSIP for all physical certificate deliveries including transfers - and for all depository book-entry deliveries. The full BASIC committee endorsed the proposal, and with the concurrence of various industry organizations, CUSIP was mandated by concerned self-regulatory bodies.

These vitally important steps proved to be the underpinning of all subsequent automation efforts that facilitate the processing of the billions of securities that are currently being traded each day.

The Proposed Machine-Readable Stock Certificate:

In June 1966 the ABA’s Security Imprinting and Processing (“SIP”) Task Force was established as an adjunct to the CUSIP effort to consider a machine-readable stock certificate. In July 1968, SIP issued its “Status Report” outlining its extensive work on the subject, concluding that a suggested 8 1⁄2 x 11” certificate that would use optical character recognition (OCR) fonts for CUSIP numbers, certificate numbers and amounts had too many problems – chiefly, the very significant technical limitations of the OCR equipment at the time.

The alternative they proposed was a punch-card stock certificate, with 22 of its 80 columns of punched data to be reserved for describing the issue, the quantity and the certificate number - and with an engraved (intaglio) vignette to be embossed on it for security. Much heat and little light was shed on their proposal…and, in a major setback, the elaborate engraving and embossing process that was used in the prototypes caused the IBM card to stick together and to jam the reading machines.

The principal advocates were brokers who saw an easy way to count and control their vault inventory and log certificate movements in and out of their firm. Federated Bank Note Company, a British firm, imprinted thousands of engraved certificates (with a bust of Churchill, which incidentally, failed to play well with many players in the American market) for testing by brokers. It saw an opportunity to crack the U.S. market dominated by the American Banknote Company and the Security Columbian Banknote Company. Meanwhile the NYSE conducted a survey of corporate issuers with varying comments returned. BASIC retained North American Rockwell (NAR) to analyze the technologies and the certificates’ OCR machine-readability. Its conclusion was that OCR could be made to work.

“Counterfeitability” was also a major concern for BASIC. Xerox had recently introduced color-copying machines, and at one of the Congressional hearings, most legislators took the “Xeroxed copies”, instead of the officially required “engraved” certificates, to be the “real ones”. An independent consultant was retained to help evaluate the banknote companies estimate of the time and cost to convert to the two versions of certificates. Its Task Force conducted interviews and analysis, publishing and distributing some 1500 copies of a discussion paper on September 9, 1970, after approval by BASIC. It advocated the OCR version. Fifty-nine responses were received. Some were quick and sharply critical, especially from the many who advocated the punched card version.

Faced with this opposition, the BASIC Task Force tested both the OCR and the punched card certificates and found them both startlingly wanting. An OCR conversion would have required re-engineered certificates, similar to existing certificates, but slightly larger. The punched card certificates (with Churchill’s vignette) had been printed two years earlier and stored in a regular office environment with no special attention given to heat or humidity. The Task Force’s tests showed that these cards did not behave in a normal manner when fed through machines. The intaglio printing had, according to IBM who helped test the cards, caused the card’s fibers to be crushed, but only in the engraved areas of the vignette and the card’s engraved border. The engraved (crushed) portion of the card did not absorb ambient humidity; the un-engraved portion behaved normally, absorbing humidity and swelling (imperceptibly) which buckled the card, albeit slightly. The cards repeatedly jammed in machines. In one dramatic case, fortuitously at the computer center of a prominent broker who was a big supporter of the card approach, the cards from a test deck literally flew out of a high speed read- er as they passed over its exposed horizontal feeder belt, landing all over the floor – Bernoulli’s airplane-wing lift effect. As it happened, the vendor’s maintenance man was present. He was told to check to see that the reader was properly aligned, which he did. It was. Rerunning the test changed nothing. The punch card certificate’s future died on the floor of his computer center. The Task Force member was asked whether he would report this back to BASIC. The answer was, “Of Course.” No tears were shed among the issuers, most transfer agents or the other banknote companies.

[Interestingly, the failure of the punch-card certificate turned out to be a very good thing. The fairly rapid expansion of “computer memory” made punch-cards – with only 80 columns in which to install a singe ‘bite’ of data per column - totally obsolete in just a few years. Meanwhile, a few transfer agents began to imprint certificate numbers, amounts and sometimes actual account numbers in OCR font on the certificates they issued - strictly on their own – even though fast and reliable OCR readers had not yet been developed. Ultimately, this saved them countless hours of error-prone ‘key-stroking’ down the road.]

FOUR UNIFORM FORMS: Forms used for settling trades and for related transactions like transfer instructions had been “personalized” since the days under the buttonwood tree and ‘on the curb’. Since no two were alike, recipients’ clerks had to search around the compass for each bit of information – to find it and manually “key it in”. This was time consuming and error-prone. In addition, if a delivery was to be effected through CCS, the originator had to print out his own form and then transcribe, usually by hand, the data needed by CCS’s clerks for computer entry. This transcribing - with all its time, cost and errors - occurred many thousands of times a day. (Later, as CCS grew, it would happen tens of thousands of time a day). As one broker put it, “the plumbing industry was 40 years ahead of the securities industry when it came to having specific minimum specifications for the outputs of a variety of producers.”

BASIC’s Task Force studied the matter as it applied to: Delivery Bills, Comparison Forms, Transfer Instructions and Reclamation Forms. In the summer of 1971, it distributed 2500 copies of a white paper on its findings and proposed sample forms to members throughout the financial community, requesting comment. Predictably, the reaction was largely a “Tower of Babble” with many of the 65 respondents questioning the need for uniformity in some or all of the four forms while others declared that if there was to be a standardized form, their own form should be considered the best and only one.

Undeterred, BASIC considered their responses, made some refinements to the forms and decided to proceed towards mandating them. Part of BASIC’s logic was that such standards would eventually lead to standards for computer-to-computer versions, thus reaping huge cost savings over and above those mentioned above.

At its December 22, 1971 meeting BASIC decided to proceed - and recommended the adoption of all four forms, with mandatory use dates of September 1, 1972 for the Transfer Instruction and Reclamation forms and December 1, 1972 for the Delivery and Comparison forms. One change, important to the transfer agent community, was that the back of the certificate (which, it should be noted, already HAD very standardized wording, so that is WAS a “standardized form” in itself) could serve as a substitute for a separate transfer instruction. With that provision, the transfer agents were in full agreement.

AUTOMATED TRANSFER INSTRUCTIONS: The uniform transfer instruction became the logical lead-in to what became known as the “magnetic tape transfer instruction” - produced by the broker, passed through DTC and consolidated by them, issue-by-issue, then sent to the transfer agent for a totally automated issuance of new stock certificates and a subsequent automatic update of its computer records - all done with virtually no human intervention. BASIC’s belief that standard forms would lead to automation of those transactions, as mentioned above, was affirmed.

The initial kick-off of automated transfers was a BASIC Ad Hoc Transfer Standards Committee, formed in November 1971, consisting of:

Bertram W. Roberts, Chairman

Nicholas J. Arrigan

John J. Britt, Jr.

Glenn A. Deppler

Charles J. Horstmann

Leonard J. Mastrogiacomo

Robert J. McCausland

James E. Osborn

H. Frank Pearson

George R. Reis

Frank W. Shelton

George C. White, Jr.

Affiliation

Morgan Guaranty Trust Company

NYSE

Merrill Lynch,

Pierce Fenner & Smith, Inc

First National City Bank

NYSE

Manufacturers Hanover Trust Company

Shields & Company

General Motors Corporation

Donaldson, Lufkin & Jenrette, Inc.

Bache & Company

American Telephone and Telegraph Co.

Chase Manhattan Bank

Members of BASIC’s Task Force provided liaison, drafting and other support for the committee.

After five months of meetings and much liaison with the rest of the brokerage and transfer agent communities, on June 30, 1972 BASIC issued the committee’s white paper, “A Proposed Standard for Transfer Instructions on Magnetic Tape”. It was universally acclaimed as a milestone in the automation of post-trade processing, promising large savings in transfer agent data entry, far greater accuracy and greatly improved transfer turnaround times.

Nevertheless, as with other attempts at industry-wide conversions, the standard format was met with a less than enthusiastic response. An Alphonse-Gaston act developed between brokers and transfer agents, with each one advocating that the other convert to their own standard customer-name and address format. Manufacturers Hanover Trust (widely known as Manny-Hanny) and Merrill Lynch were the first two players to say, let’s just do it. And they did.

But it took over two years before the bigger, industry-wide logjam was broken; DTC, the central hub through which most transfer instructions passed from brokers on their way to transfer agents, took on the task of applying new and highly innovative software to convert the myriad broker formats into a single standard, built around BASIC’s 1972 proposal. Twenty years later virtually all broker- originated transfer instructions were fully automated.

The “Direct Mail Program”: By this time – after yet another groundbreaking “handshake agreement” between Manny Hanny and Merrill Lynch, with compensation to be based on the very obvious labor savings that could be and were realized – most brokers and transfer agents had begun to collaborate on a “direct mailing service” where transfer agents mailed newly issued certificates directly to the brokers’ customers, with a standardized “cover letter”, rather than having them returned to the brokers for mailing. Now, certificates could be produced and mailed - basically untouched by human hands – saving large amounts of largely manual labor, to sort and deliver stock certificates to the brokers who’ve requested them, and many days in terms of getting the certificate to the customer. (Kudos to Ray Riley of Manny Hanny, who soon went on to be president of the Stock Transfer Association, at a very critical juncture, and Ralph Roth of Merrill Lynch, who got his ‘big boss’, then Merrill’s Chief Operating Officer, to sign on to the idea with a simple handshake). [In another historical aside, Riley was written-up by the Bank’s outside auditors for not having a written contract in place when they conducted the annual audit].

Other Initiatives Taken to Modernize the Security Industry Taken by BASIC and DTC

The Omnibus Proxy: One of the most important areas of corporate governance is to assure prompt, efficient issuer-investor communications. In DTC’s early years, the increase in retail- investor-owned stock deposited in DTC by member brokers raised fears, with good reason, that DTC would be yet another intermediary that would impede the proxy mailing and voting process by creating too many hand-offs. Proxy materials would be delivered by the issuer’s agent (usually its transfer agent) to DTC - who would distribute them to brokers - who would then pass them on to their customers (beneficial owners) - who would vote via individualized proxy cards, return them to the broker, who would return them to DTC for redelivery to the agent. Clearly, this was a process that was badly in need of streamlining.

After much consultation with leaders of the American Society of Corporate Secretaries, representatives of the Stock Transfer Association, and with regulators, DTC developed its highly successful Omnibus Proxy (OP) service.

This service, implemented on January 1st 1975, reduced to a minimum the presence of Cede & Co. (DTC’s nominee name) between issuers and DTC members in connection with the voting of shares registered in Cede’s nominee name. Under the new procedure, DTC delivers an Omnibus Proxy to the issuer immediately after record date. This is now fully automated. The OP in effect assigns to each member having shares in the issue on deposit in DTC on record date, the voting rights DTC is entitled to for all such members. Each such member is simultaneously notified of the submission of the OP and the number of shares it is entitled to vote. The issuer receives the same voting entitlement information. Thus the member is able to ask the issuer (or its agent) for the number of proxy cards and proxy materials necessary for the member to satisfy its responsibilities to the beneficial owners of the shares. The voting results are submitted directly from the member to the agent. Thus, DTC is completely removed from the chain of communications between the issuer and the beneficial owners.

FINS: BASIC’s main initiatives, described above, were followed by work on a Financial Industry Numbering Standard (FINS) - as a way to uniquely specify contra-parties to transactions. (It’s equivalent to the way CUSIP uniquely identifies securities issues). FINS was eventually taken over, implemented and maintained by DTC.

The COD-DK Problem: BASIC spent much staff time considering solutions to the paralyzing and costly “COD-DK problem”. (COD stands for Cash - or Collect - On-Delivery and DK (which clerks used to scrawl, or sometimes stamp with a rubber stamp (!) on each form they rejected) stands for I Don’t Know this incoming delivery and therefore I’m rejecting it back to the sender.) This problem was a major contributor to the paperwork crisis. While BASIC was never able to fully resolve the problem, since “not knowing” a trade” was and still is a ‘legitimate way’ not to promptly pony-up money, it did lay the groundwork for DTC’s immensely successful Institutional Delivery (ID) System, introduced in 1973. Since most traders DO know the trades they’ve made – and DO want to settle them in timely fashion, it is now universally employed to connect all parties, electronically, through DTC, to effect reliable settlement - saving the financial industry hundreds of millions annually vs. what they used to spend to manually match-up trades and settlement arrangements or “D-K them” - only to have them come back a second time.

The ID solution to the DK problem had its own Alphonse-Gaston act. The institutions’ traders wanted the brokers to use it before sign- ing on and the brokers made the same demands. While many far-seeing ID users on both sides used ID profitably, growth in total participation stalled at about 50% of potential users leaving too much exception processing for both sides. In 1981, under encouragement from the Security Industry Association’s Operations Committee, the NYSE adopted Rule 387, mandating the use of ID for all institutional customers wishing to maintain the COD privilege. The SEC approved the Rule a year later. DTC assembled a 30-person task force of member volunteers to train users in ID procedures across the country, and a year later and with several million dollars spent, the full conversion was completed so that all the many thousands of COD institutional customers were effective ID users, as were the hundreds of brokers doing business with them. Savings to the industry were reported to be nine-figures annually. As trading volumes exploded later in the 1980s all agreed that universal ID use saved the industry from gridlock and catastrophe.

Easing Access to DTC for Users around the U.S. and the World: In 1971, BASIC formed an “Ad Hoc Communications Committee” to study using electronic communications as a way of facilitating access to CCS’s – and later DTC’s - New York computer center. This committee, supported by the Task Force issued a 50-page report to the DTC user community, providing a conceptual framework that eventually led to today’s massive communications network, connecting depository users around the world.

THE RISE - AND FALL - OF REGIONAL SECURITIES DEPOSITORIES: During DTC’s early evolution, other financial centers with stock exchanges - with BASIC’s encouragement - developed their own versions of DTC; such as the Mid-West, Pacific and Philadelphia Securities Depositories. This collaboration, under the aegis of the NCG for CSDSs (described earlier), helped reassure the Government and the other markets that DTC would not become a monopoly, controlled by the big New York banks and brokers with the goal of putting regional firms out of business. By the 1990s however, these depositories began to conclude that they did not have, nor were they likely to gain, the critical mass of volume needed to sustain their independence and they voluntarily transferred their business to DTC, usually for a payment from DTC for their revenues and their customer relationships. As I write this, all of the region- al depositories have been folded into the “central depository” model that Herman originally envisioned, and all the “regional stock exchanges” have disappeared as well.

About the author: William F. (Bill) Jaenike, who was one of the original BASIC Task Force members, went on to become the second Chairman and CEO of DTC. Following his retirement he served on the boards of several organizations and, more recently - following multiple trips to Latin America, and extensive research on his own - he published “Black Robes in Paraguay-The Success of the Guaraní Missions Hastened the Abolition of the Jesuits ”- which describes the thirty vast and highly sophisticated mission-cities that Jesuit missionaries founded in 17th and 18th century Paraquaria, and how the commercial success of these complexes led to the forced deportation of thousands of Jesuits, both in Latin America and in Europe and ultimately, in 1773, to the pope’s worldwide liquidation of the Jesuit order. Visit www.barnesandnoble.com to read the universally favorable reviews it has received and to purchase a copy. Or, to obtain a signed copy, contact Bill directly at WJaenike@aol.com

Share

Share the Optimizer with your colleagues!