Thanks much to our colleagues and friends Pat Tracey and Andy Wilcox, who alerted us to the Mercury Vote website, advising that:

“We are an auction marketplace that empowers shareholders to generate extra revenue by selling their unused proxy voting rights,enabling investors to obtain these aggregated proxy votes to reduce costs.”

There’s not much info on the website yet, other than the callout message and photos of the Management Team, led by Spencer Huckleberry Hurst (how’s that for a moniker that makes you look twice? - which led some folks to suspect a prank) who is a recent Cornell grad, and who is already well-along with this project. And the timing sure is perfect if you think, wrongly, that “Shareholder Votes Have No Value” – OR who know they DO but try to grab them up for nothing.

There is, we can assure you, an already active “dark marketplace” that allows investors to buy and sell votes, as we believe they should be allowed to do, But only with proper disclosures we say, and with a foolproof way to deliver legally binding votes to the buyers. There’s a group of people who regularly borrow money to buy blocks of stocks before the record date for upcoming proxy fights they’ve often launched themselves. Then, typically, they sell them as soon as the fight is announced, and laugh all the way to the bank.

And there are many other ways to capture voting rights on the Q-T besides. Selling votes on the QT is a huge moneymaker for retail brokers, whose margin agreements allow them to sell client’s votes - with no notice to them, and without a penny of compensation - even if they have never had a margin balance.

There really is a lot of work to do “behind the scenes” to actually capture peoples’ voting rights and conduct an “auction” to arrive at the price. In short, you really need to get a legally binding “Irrevocable Proxy” that’s good until the Meeting is officially concluded, then to get bidders for the votes themselves. But when we look at the big money spent by both sides to round up votes in a proxy contest – and when one looks at the stakes – which often decide the FATE of the targeted companies - and their Directors - one can easily imagine that both sides will be tempted to outbid – or outfox the other to eke out a victory at the polls, whatever the costs may be.

We wish every success to Mercury Vote – although we also need to note that an earlier venture like this – Shareholder Vote Exchange – was successfully launched in 2021 – but folded shortly thereafter.

Sell Your Proxy Votes? Good Idea, We Say, But Lots Of Practical Problems | Optimizer Online

This article also contained even more info to prove that Shareholder Votes Have Value (like the big stock-price premiums that accrue to shares with supermajority votes in a proxy fight) – which Exxon Mobil and its advisors would be wise to bone up on. How about a 32.7% premium ($7.05 per share) on a super-voting class of stock in the runup to a threatened proxy fight at Paramount Global?

And Speaking Of Proxy Fights…

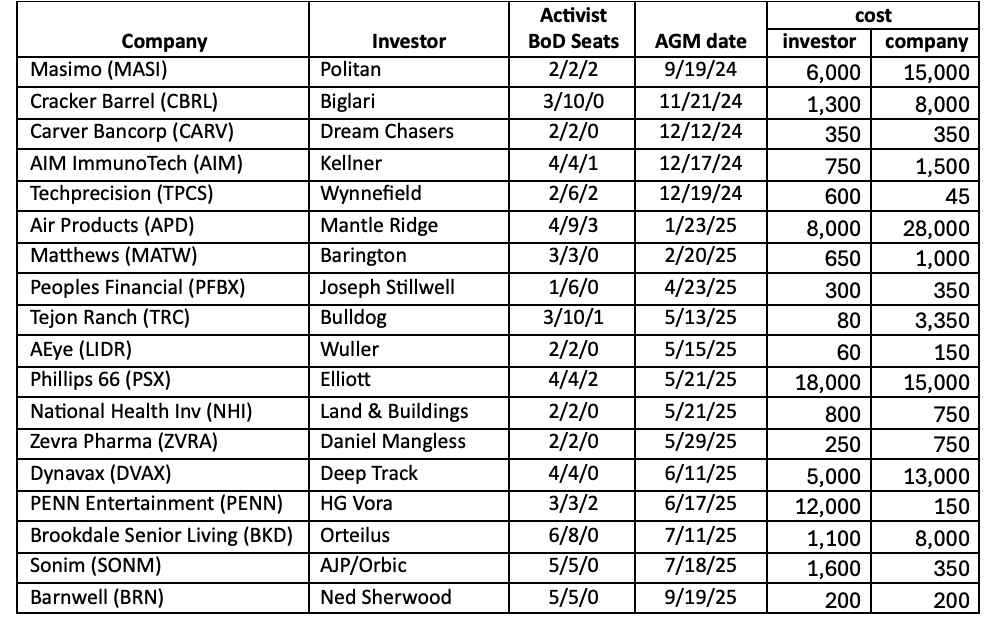

Through September, there have been 17 proxy contests in 2025 “that went as far as an actual shareholder vote under universal proxy” rules, according to the Oct. 6 posting by The Activist Investor, which avidly tracks proxy fights. Of the 17, seven – or a very robust 41% of the contests - saw the activists winning one or more seats.

TAI also looked at the costs involved, noting “It’s not cheap to exercise your rights… Activists, both very experienced and new, have started to spend some serious money on them.”

“On average across the seventeen contests, activists spent an average of $3.2 million. Companies spent an average of $5.3 million. We see an enormous variance in spending, though… The most expensive contest was at APD, where [the contenders] spent a combined $34 million.

Source: The Activist Investor

Source: The Activist Investor

“We must note these figures are at least kind of rough,” TAI observed. “Companies and activists disclose an estimated ‘cost of solicitation’ in a definitive proxy statement, following SEC guidelines. The SEC does not audit or even review this figure, though. Companies and activists alike set forth figures that in part reflect strategic moves. Some say they plan to spend a considerable amount [“hoping” we’d say] to intimidate the other or draw them into spending even more. Others might say they plan to spend a minimal amount to encourage complacency.”

In most fights, the company side spends a great deal more than they report – on things like opposition research, legal “consulting,” “outside advisory bills” and public relations efforts that are not counted as “solicitation expenses” by the SEC. All grist for the mill, we say in terms of Shareholder Votes having very significant VALUE. The proxy fight tally is pretty much done for 2025 – with another five fights still “in the hopper” – all of them where the activist is looking to win a majority of the open seats – for a grand total of 22 Fights in all.

Share

Share the Optimizer with your colleagues!